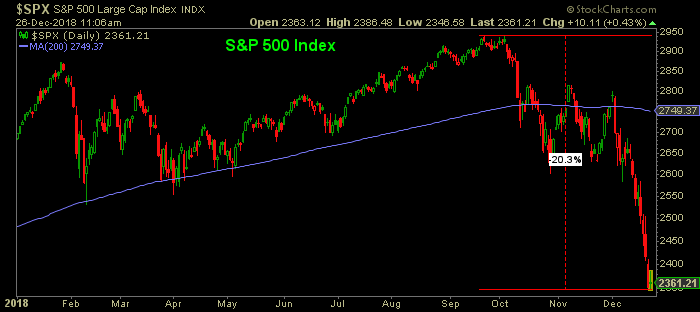

It's official: the bear market of 2018. Like many of the previous bears, it's been an elevator down, with a 20% decline in just 3 months.

The question many are asking: Is this decline just a decline or is it signaling an oncoming recession?

Looking back at history, the answer is far from clear. This is now the 21st bear market since 1929. Of the previous 20, only 11 were associated with a recession (55% of the time).

The list of bears with no recession is probably longer than you would have guessed...

What gives? Isn't the stock market a "leading indicator" of the economy? Yes, it can be at times, but it's far from a perfect one.

Sometimes a bear is just a bear. Is this one of those times? We'll only know in hindsight.

Looking at the data, the U.S. economy does not yet appear to be in a recession, but that fact is hardly an all-clear. After the March 2000 stock market peak, a recession did not begin until a year later: March 2001. No one can say for sure that in September 2019 (a year from the September 2018 S&P 500 peak) there won't be a recession.

And so, we wait, evaluating the evidence as it develops. If a recession is coming, the odds favor a longer and deeper bear market (-42% over 17 months on average). But there's much variation within those odds... In the 1990-91 recession, stocks declined only 20% over a 3-month period, and during the 1929-33 depression, stocks declined 86% during a 33-month period.

So while unlikely, a recession could be coming without any further stock market declines. It's safe to say that most investors are probably not thinking about a repeat of the 1990 scenario. They are most likely assuming the 50%+ recessionary bear markets of 2000-02 and 2007-09 are the norm. While a repeat of these calamities is certainly possible, so is a much shallower bear market and recession, or no recession at all.

In markets, every time is different. 2018 has proved this maxim once again.